A shotgun clause is among the strongest but most risky provisions in a shareholder agreement. Alternately referred to as a buy-sell provision, this provision can either be your business partnership’s savior in the midst of disputes that cannot be reconciled or the very provision that facilitates your untimely departure from the company you helped establish. Knowing how these clauses work, when to employ them, and their possible drawbacks is something any business owner in Ontario needs to know.

What Is a Shotgun Clause?

A shotgun clause is a provision in shareholder agreements that is typically inserted and allows shareholders to sell or purchase their shares under certain conditions. The clause owes its name to its speedy and surefire character similar to a shotgun blast, where once initiated, the effect is instantaneous and irrevocable. Essentially, a shotgun clause permits a single shareholder to offer to buy another’s shares at a stated price. But the shareholder receiving the offer has a choice: take the offer and sell their shares, or “turn the gun around” and buy the offering shareholder’s shares at the same price. This special mechanism guarantees that the individual issuing the offer has to be willing to buy or sell at what they quote. The clause is both a dispute resolution mechanism and a tool for pricing, intended to allow for a clean break when shareholders are unable to continue working together. In Ontario’s business environment, these clauses are most useful for closely-held corporations where shareholders regularly work together on a day-to-day basis and personal relationships have the potential to play a big role in business operation.

How Does a Shotgun Clause Work?

The operation of a shotgun clause is in a simple but important procedure that any business owner should know prior to consenting to incorporate such provisions into his or her shareholder agreement.

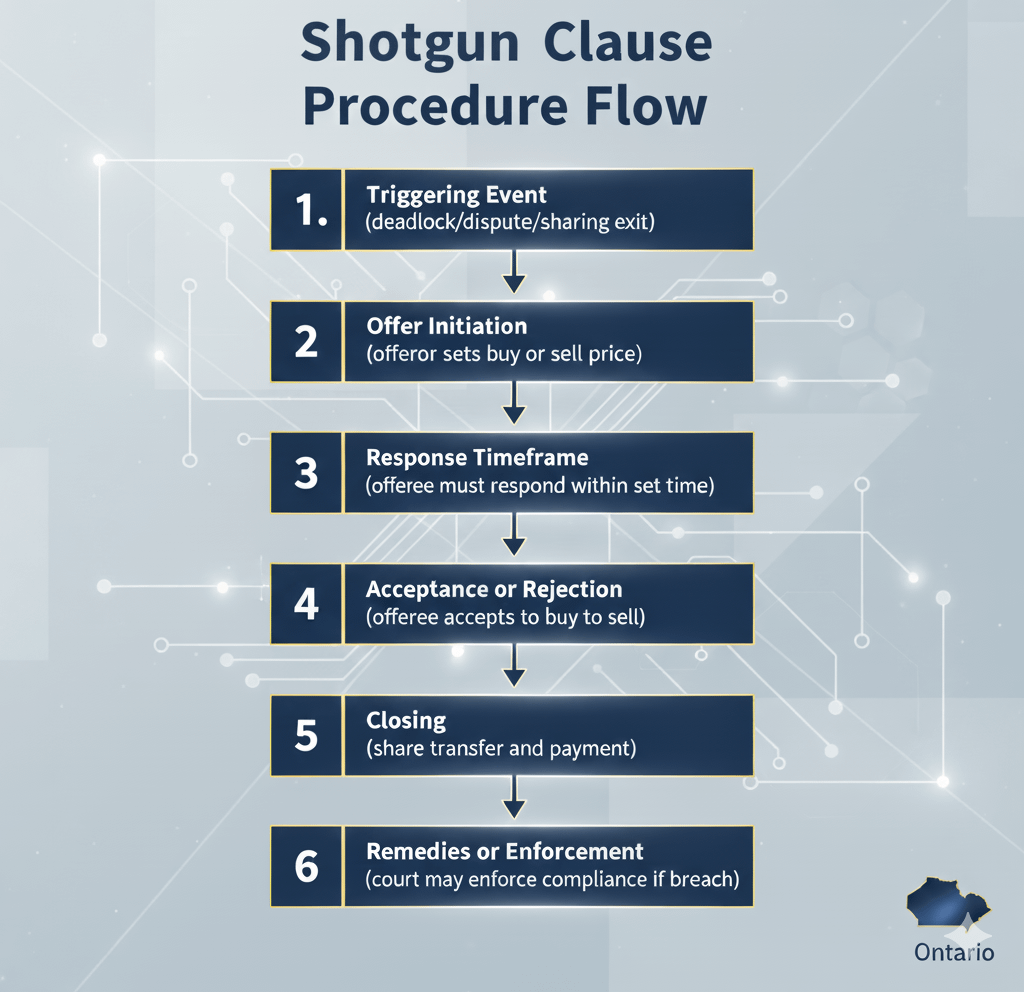

Procedure Flow for How a Shotgun Clause Functions

Here is a brief flowchart description of the shotgun clause procedure in Ontario:

Triggering Event (deadlock/dispute/sharing exit)

↓

Offer Initiation (offeror sets buy or sell price)

↓

Response Timeframe (offeree must respond within set time)

↓

Acceptance or Rejection (offeree accepts to buy or sell)

↓

Closing (share transfer and payment)

↓

Remedies or Enforcement (court may enforce compliance if breach)

The Trigger Phase

A shotgun clause may be initiated by any one of several events or situations as spelled out in the shareholder agreement. Some of these common events are:

- Irreconcilable disagreements between shareholders

- Deadlocks where key business decisions are not possible

- The wish of one shareholder to leave the business

- Shareholder agreement breach

- Loss of faith among business partners

The Offer Process

When a shareholder chooses to exercise the shotgun clause, they are required to give written notice to the other shareholder(s) of their desire to purchase the shares of the other party or sell their shares at a certain price per share. The offer must be in writing, unambiguous, and contain all necessary terms like the price of purchase, payment method, and closing date.

The offering shareholder has no idea whether they will wind up selling or buying, thus inducing them to pick a reasonable price. They can’t offer too cheaply, lest the other shareholder take the reverse bid and pay them off at that low level. They can’t offer too expensively, or they will be paying more than they had wanted to.

The Election Period

As soon as the shotgun offer is proposed, the receiving shareholder usually has a certain period of time (ordinarily 30 to 90 days) in which to decide. During this period of election, the receiving shareholder will have to make a choice between:

- Accepting the offer to sell: selling his shares to the offering shareholder at the stated price

- Reversing the offer: purchasing the offering shareholder’s shares at the same price

- Do nothing: which generally amounts to being held to have accepted the offer to sell

Irrevocability and Binding Nature

Recent case law, such as the British Columbia Court of Appeal ruling in Blackmore Management Inc. v. Carmanah Management Corporation, has established that shotgun offers are usually irrevocable as soon as made. The offering shareholder can’t then withdraw their offer merely because market conditions shift or they change their minds regarding the price they offer.

The Benefits of a Shotgun Clause in a Shareholder Agreement

Shotgun clauses provide several strong benefits that make them appealing to owners of businesses who wish to safeguard their investments and maintain continuity of business.

1. Efficient Dispute Resolution

One of the main advantages of a shotgun clause is that it can end deadlocks rapidly and effectively. When shareholders deadlock on key business issues, usual means of dispute settlement such as negotiation or mediation may be insufficient. The shotgun clause offers a clear-cut solution which compels agreement so that the business can continue operating under unambiguous management.

2. Fair Pricing Mechanism

The Shotgun Clause structure uniquely encourages equitable pricing. Because the offering shareholder will have to buy or sell at the price they will set, there is tremendous incentive to offer a good market price. This built-in regulating device prevents lowball offers or fantasies that could happen in other exit circumstances.

3. Protection of Business Continuity

Unlike other mechanisms of resolving disputes that could lead to business dissolution or prolonged court cases, shotgun clauses enable the business to keep running with a definite structure of ownership. The procedure usually leaves one of the parties acquiring full control as the other walks away cleanly without any uncertainty and disputes hurting business operations.

4. Cost-Effective Resolution

Relative to lengthy arbitration proceedings or litigation, shotgun clauses are a relatively cheap means of settling shareholder disputes. The process is streamlined to avoid high legal costs and business interruption, as is especially the case with small to medium-sized enterprises where drawn-out disputes would be financially crippling.

5. Prevents Minority Oppression

In well-designed agreements, shotgun clauses can shield minority shareholders against majority oppression. Minority shareholders are given a clear mechanism to exit when they perceive their interests being unjustifiably overlooked through a shotgun clause, while majority shareholders are given an avenue to fully control if they feel it is in the best interest of the business.

The Risks of a Shotgun Clause in a Shareholder Agreement

Despite their benefits, shotgun clauses carry significant risks that business owners must carefully consider before including them in shareholder agreements.

1. Financial Imbalance Issues

Perhaps the most significant risk of shotgun clauses is their potential unfairness when shareholders have unequal financial resources.

A financially stronger shareholder may strategically trigger the clause knowing that their partner lacks the resources to reverse the offer, effectively forcing a sale at below-market prices. This was illustrated in the Ontario Court of Appeal case Western Larch Limited v Di Poce Management Limited, wherein several shareholders pooled their means to expel one partner.

2. Valuation Challenges

Valuing a private company can be very challenging, especially in times of distress or uncertainty. If the offering shareholder overestimates the value of the company because of limited information or volatile markets, the consequences are financially catastrophic. The COVID-19 pandemic, for instance, created circumstances where business values were wildly different, and there were controversies over shotgun offers made prior to market changes being realized.

3. Information Asymmetry Risks

Shotgun clauses can be especially problematic when one shareholder knows a great deal more about the business than others. An operating shareholder involved in the day-to-day affairs of the business may have information regarding upcoming opportunities or issues that an investor lacks. Information advantage can then be used to make shotgun clauses trigger at strategic times and produce unfair results.

4. Emotional and Relationship Fallout

The forcefulness of shotgun clauses can aggravate disputes and irrevocably harm relationships among erstwhile business partners. In contrast with cooperative approaches to conflict resolution, the “all-or-nothing” strategy of shotgun clauses may further heighten emotions and preclude cooperation in the future, which can be especially difficult in family businesses or partnerships with emotional relationships.

5. Timing and Market Risk

When activated, shotgun clauses make use of tight deadlines that do not consider market instability or timing matters. A shareholder might end up having to make a pivotal choice at adverse market conditions or when unable to secure proper funding. The Blackmore case demonstrates how outside occurrences such as a pandemic can cause unexpected challenges in shotgun procedures.

Common Mistakes to Avoid with Shotgun Clauses

Being familiar with the pitfalls of shotgun clauses helps businesspeople write more effective contracts and save time and money.

1. Establishing Unacceptable Trigger Prices

The most common error is establishing offer prices without due regard for their reasonableness from the buyer’s and seller’s points of view.

The case law is replete with instances of shareholders making lowball proposals hoping their partners will sell, and then getting bought out at their own unwholesome price.

Business owners ought to ask themselves at all times: “Would I be happy buying at this price, and would I be happy selling at this price?”

2. Inadequate Valuation Provisions

Most shareholder agreements do not outline explicit valuation methods for shotgun bids. Since there are no predetermined methods of valuation or professional appraisal requirements, it is almost certain that there will be disagreements about fair price. Best practices involve mandating independent business valuations or setting well-defined formulas based on financial indicators.

3. Oversight of Financial Ability Disparities

Compilation of shotgun clauses without regard for the comparative financial capabilities of shareholders is a recipe for inequity. When a shareholder far exceeds others in terms of finances, the clause turns into a means for oppression and not equitable resolution of disputes. Protective provisions or other mechanisms should then be contemplated in such cases.

4. Inadequate Notice and Election Periods

Hastening the shotgun procedure with poor notice periods or impractical timelines for making decisions can precipitate unjust results and legal disputes. Shareholders require ample time to secure financing, carry out due diligence, and make informed choices. Standard election times are 30 to 90 days, but intricate businesses need more time.

5. Insufficient Attention to Regulatory Mandates

Certain businesses are subject to regulatory approval for transfers of ownership, like regulated industries or professionals. Shotgun clauses that do not provide for such requirements can cause tender offers to be unable to be completed, resulting in claims of breach and further disputes.

6. Tax Implications are Ignored

Tax implications of shotgun transactions may be substantial and will depend on the nature of the transaction and the involved shareholders. Neglecting tax planning and tax cost allocation in the shareholder agreement may lead to further conflicts within an already stressful procedure.

7. Insufficient Legal Documentation Requirements

Shotgun offers must strictly adhere to the provisions of the shareholder agreement to be binding. Ambiguous or partial offer documentation can be a basis for challenge. The Western Larch case clarified that strict compliance is necessary, but not perfect compliance, but it behooves counsel to undertake thorough legal review to appreciate this difference.

Western Larch Limited v. Di Poce Management Limited (2014 ONCA 30)

Two shareholders in a logging business deadlocked over management decisions. One shareholder served a shotgun notice offering to buy the other’s shares at $1.5 million. The respondent argued the notice failed to comply perfectly with form requirements. The Ontario Court of Appeal held that the offer need only “strictly comply” (not “perfectly”) with the agreement’s terms and enforced the buy-sell provision.

FSC (Annex) Limited Partnership, 2020 ONSC 5055.

FSC (Annex) Limited Partnership (applicant) and Adi 64 Prince Arthur L.P. (respondent) were joint venture partners in a luxury condo development. Due to difficulties, the applicant triggered a shotgun buy/sell clause in December 2019. In January 2020, the respondent elected to buy out the applicant’s interest, with closing set for April 2020. In March 2020, the respondent refused to close, citing COVID-19–related financing issues. Applicant sought specific performance; respondent argued frustration and equitable grounds against specific performance.

The Ontario Superior Court of Justice held that: The respondent was bound by its election under the shotgun buy/sell clause to purchase the applicant’s (FSC (Annex) Limited Partnership’s) interest. The doctrine of frustration did not apply- COVID-19 and the resulting financing difficulties were not enough to discharge the contract. The respondent was in breach for refusing to close. Specific performance was the proper remedy, requiring the respondent to complete the purchase, rather than merely paying damages. It was observed that the respondent must complete the purchase of the applicant’s interest under the shotgun clause as agreed.

How a Business Lawyer Can Help

Due to the intricacies and high value associated with shotgun clauses, expert legal support is critical in drafting as well as enforcing these provisions efficiently.

1. Drafting and Tailoring

A seasoned corporate attorney may assist in customizing shotgun clauses to your unique business situation. This involves taking into account the number of the shareholders, their comparative financial standings, the business’s nature, and industry-specific necessities. Lawyers can also prepare defensive provisions for minority shareholders or dispute resolution arrangements if shotgun clauses are not suitable.

2. Valuation Methodology Design

Legal advice can assist in providing clear, reasonable valuation methods that minimize controversy and maximize enforceability. This may involve independent appraisal requirements, particular financial metrics, or discount/premium adjustments based on percentage ownership and market conditions.

3. Regulatory Compliance

Legal practitioners ensure shotgun provisions are consistent with applicable corporate law, securities regulations, and industry requirements. In Ontario, for instance, this means consistency with the Business Corporations Act (Ontario) and professional licensure requirements applicable to share transfers.

4. Enforcement and Dispute Resolution

Whenever shotgun clauses are activated, attorneys offer critical advice on relevant procedure, documentation, and enforcement. They can facilitate the compliance with terms of agreement while defending their client’s interests during the process.

5. Alternative Mechanism Design

Senior advice can propose substitutes for classic shotgun clauses in situations where they are not suitable. These may involve put/call options, tag-along and drag-along rights, or structured exit arrangements which are more suited to the company and shareholder dynamics.

Alternatives to Shotgun Clauses

In situations where shotgun clauses are unsuitable or ineffective in certain business scenarios, various alternative mechanisms can offer effective resolution of disputes and exit strategies.

1. Tag-Along and Drag-Along Rights

Tag-along rights provide minority shareholders with the right to join in on a sale caused by majority shareholders, so they get the same terms and price. Tag-along rights prevent minority shareholders from being left behind when majority shareholders want to leave.

Drag-along rights allow majority shareholders to compel minority shareholders to join in a sale to a third party such that the purchaser can buy 100% ownership. Such provisions are especially necessary if potential buyers need full control.

2. Put and Call Options

Put options enable shareholders to compel the company or fellow shareholders to purchase their shares at prearranged prices or formula of valuation. Call options entitle some shareholders to buy others’ shares under agreed circumstances. These arrangements offer more formalized and predictable avenues for exit than shotgun clauses.

3. Right of First Refusal (ROFR)

ROFR provisions allow current shareholders to buy shares before they are open to sale to third parties. Although not as hostile as shotgun clauses, ROFRs assist in keeping control of ownership mix and can be coupled with reasonable valuation mechanisms.

4. Professional Valuation Requirements

Certain contracts require third-party professional valuations in the event of a dispute, eliminating subjective pricing altogether. Though more costly than shotgun methods, professional valuations can yield fairer results, especially in complicated businesses or where information asymmetries.

5. Structured Mediation and Arbitration

Properly drafted mediation and arbitration clauses can achieve effective resolution of disputes without damaging business relationships. These give the option of more subtle resolutions than the stark choices of shotgun clauses and can deal with distinct business concerns without calling for total severance.

FAQs

1. What is also known as the shotgun clause?

Shotgun clauses also are used to mean “buy-sell provisions,” “buy-sell agreements,” “Russian Roulette clauses,” or “auction provisions.” Jurisdictions also use the term “Dutch auction clauses.” All these names describe the same general mechanism whereby one party offers and the other party may accept or reject the offer.

2. Is a shotgun clause always required in a shareholder agreement?

No, shotgun clauses in shareholder agreements are not required under Ontario legislation. Nevertheless, they are strongly advised for closely-held companies with more than one shareholder, especially where shareholders hold equal ownership interests. The use of a shotgun clause ought to be contingent on the unique situation of the business and shareholder-to-shareholder relationship.

3. Can a minority shareholder invoke a shotgun clause?

Yes, minority shareholders can usually initiate shotgun clauses, but this is frequently impracticable because of the financial implications. When a minority shareholder issues an offer, the shareholder should be ready to buy the majority shareholder’s larger holding at the price offered. This tends to involve a far greater amount of money than the minority shareholder has at his or her disposal, so that the clause is not such an effective protection mechanism for minorities.

4. How is the price set in a shotgun clause?

The offering price under a shotgun clause is to be decided by the offering shareholder but must be identified in the agreement as to how this price is to be determined. Best practice is to mandate independent valuations, to utilize pre-agreed formulas based on financial metrics, or to have definite guidelines for determining fair market value. Some agreements mandate that the offering price be at fair market value, but others permit absolute discretion to the offering party.

5. Are shotgun clauses enforceable in Ontario courts?

Yes, shotgun clauses are normally enforceable by Ontario courts, as long as they meet the precise terms of the shareholder agreement and the requirements of law. In Western Larch Limited v Di Poce Management Limited, the Ontario Court of Appeal held that shotgun offers are required to “strictly comply” with agreement terms, although this does not mean “perfect compliance.” Courts will enforce well-drafted and properly executed shotgun provisions but grant remedies for technical shortcomings in minor respects in the form of damages.

6. What are options if shareholders do not want a shotgun clause?

There are a number of options available to shareholders who do not wish to have a shotgun clause:

- Tag-along and drag-along rights for more organized sale processes

- Put and call options with formulas for fixed prices

- Professional mediation and arbitration provisions for cooperative dispute resolution

- Buy-back provisions enabling the corporation to buy back shares.

- Right of first refusal provisions in order to manage ownership transfers

- Structured exit mechanisms with professional valuations and payment terms

The alternative to be chosen will depend on the company structure, shareholder relationships, and level of protection desired by different parties.

Conclusion

Shotgun clauses are effective mechanisms for dealing with shareholder conflicts and business divorces but need proper consideration, professional drafting, and effective implementation.

Ontario business owners contemplating these provisions need to consult closely with qualified corporate lawyers to ensure that their shareholder agreements contain suitable protections while realizing their business goals. Schedule a consultation with our corporate law team today to review your agreement and protect your investment.

Regardless of whether you decide to have shotgun clauses or implement other mechanisms, the most important thing is to have well-defined, equitable, and enforceable terms that confront the realities of your particular business arrangement and safeguard all legitimate interests of shareholders. Contact us today to draft, review, or update your shareholder agreement with confidence.